Tricks Of The Trade

March 2021Interest free credit mattresses & beds exposed – why 0% credit isn't free

Updated 2021: No doubt you’ll have seen a flashy advertising campaign or two, shouting at potential customers to ‘buy now, pay later’ with ‘no deposit needed’. It can be a tempting draw for those who are a little tight on money; but do we really understand how interest-free credit mattresses and beds work and what long-term value we are getting from it if any? Have you been tempted by 0% finance mattresses offered by the big retailers?

Is there ever an interest-free deal to be had or are we all being scammed by the finance companies?

This article will explain the somewhat shocking hidden fees that all shoppers are subject to when they buy a mattress from a company that offers interest-free credit.

- Who pays for interest free credit?

- Why interest-free credit isn’t free

- How does interest-free credit work?

- Why we no longer offer interest free credit

Who is losing out with interest-free credit?

The purpose of interest-free credit is to remove any doubt in the customer’s mind that they can afford a new luxury item right now, regardless of financial situation or their best judgement.

In reality, the total price the customer agrees to pay is considerably more expensive than it should be with the hidden cost of credit factored in, so you end up investing in a deal that isn’t a ‘bonkers bargain’ at all.

In the above example, customers who take credit for financial reasons are paying £180 (15-20%) straight away on top of what they should be paying. Because the cost of interest is effectively hidden, the customer doesn’t realise when they are being over-charged or that the mattress quality has been reduced to absorb this charge.

Even worse than that, customers who choose to pay £1,000 upfront to purchase the bed (and therefore do not need IFC) are still being charged for the additional cost of credit – despite the fact that they are buying the bed outright. These people are getting the worst value for money imaginable! Try asking a retailer for a cash discount and we bet there is no such option to remove the finance charge of £180.

This is the same with all interest-free credit offers, whether it’s curtains, kitchens, bathrooms, the list goes on. It all boils down to a simple sales tactic, where the deal is often more appealing than real value for money or the quality of the product.

Interest-free credit is not free credit

When looking for a mattress on interest-free credit the first thing to remember is there is no such thing as free credit. You may feel perplexed by that, surely it has to be free? Let’s look a bit deeper at how the pricing structure keeps this hidden from you the customer. The simple fact is that the total cost of your mattress when buying on credit has already had the ‘interest charge’ added by way of front-loading this on to the retail price. For everyone no matter if you take the credit or not.

Unfortunately, there’s no such thing as a free lunch, and no finance service will lend you money without making some profit on it themselves.

Shocking isn’t it? You’re literally paying for everyone else’s credit even if you don’t use it!

There is no such thing as a free lunch, all credit charges are hidden within the price

Retailers offering interest free credit have already factored the cost into the price to begin with

How interest-free credit actually works with beds

Interest-free credit is big business with finance companies making 8-15% off all sales when customers choose it. These fees are always baked into the price of the good your buying, whether you take the credit or not.

The ins and outs of interest-free credit mattresses (IFC) can get quite confusing. So let’s break it down using the fictional retail mattress. The Super-Dreamy 1000 pocket sprung mattress will be our commonly seen example.

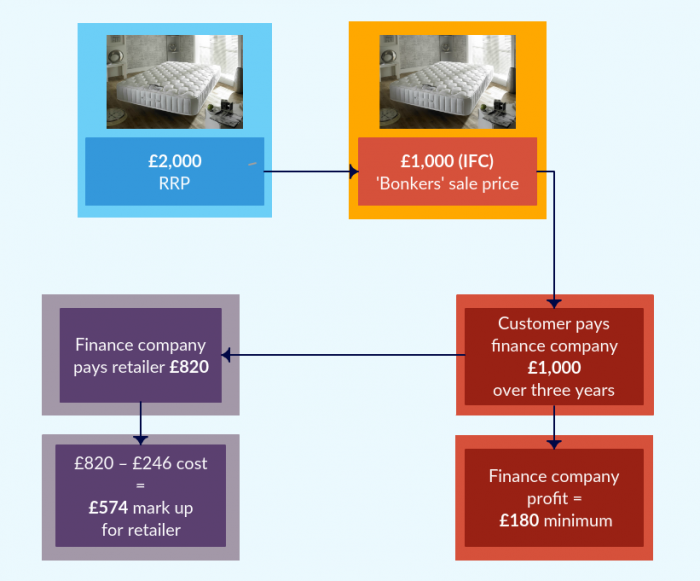

Say the mattress is advertised as part of a ‘Bank Holiday Bonkers Deal’ at £1,000 (IFC) – reduced 50% from the original £2,000 RRP. An unbelievable bargain, right?

o

Well, not exactly.

In truth, the original £2,000 RRP is not a realistic target; it’s an intentionally hyperinflated price. Retail stores can list a product at this price for as little as one week in their quietest outlet before slashing the price in half across all of their stores. The £1,000 reduction is, in fact, the realistic price they expect to sell the product at.

Typically, the retailer makes up to 70% markup – and so would usually expect to sell the mattress for around £600-£800 to cover the cost of production and all of their additional overheads. Typically the retail cost of producing the Super-Dreamy 1000 pocket sprung mattress is around £246.

Choosing the interest-free credit option when buying a mattress

Now let’s say a customer chooses to buy the mattress using interest-free credit and agrees a deal with the finance company to pay £1,000 over the course of three years.

Of that £1,000, the finance company pays the retailer £820 and takes £180 (15-20%) as their charge for the credit. This £180 is effectively the hidden cost of credit interest and the finance company’s minimum profit.

Why minimum? Failure to make repayments, or even making one payment late, means the customer is liable to pay up to 30% more in additional charges. In fact, some finance companies may work this missed payment into their metrics for profit margins, counting on a few people missing the payments and being penalised.

Why we don’t offer interest-free credit

We tried to offer interest-free credit without impacting our prices for a couple of months. Mainly for customers who may have needed a little extra help in getting their perfect mattress. However, our experiment led us to have up to 8%-15% additional fees added for each mattress. We kept the price the same without the credit fee, but these fees made it completely unworkable for us in the long term.

The credit provider was very clear that these charges should be passed onto the customer as ‘they will never know’. Totally shocking and unethical. We absorbed this 8%-15% charge for the trial period we ran with rather than adding it onto the product prices. Which would unfairly impact all customers.

It made us think just how much additional cost there is with other mattress retailers that do offer interest free credit. After 2 months we removed interest-free credit as its totally unsustainable. It gave us a look into the really murky world of interest free credit which we want no part of.

Buying from an independant mattress retailer will provide far higher quality components without hidden fees

By avoiding interest free credit you’re ensuring your money is spent purely on the mattress components

How to get a good deal on a mattress without using credit

At John Ryan By Design you will be dealing with us and only us, no third party creditors or suppliers adding to the cost.

Rather than regurgitating all the typical sales mumbo jumbo, our Outlet section offers immediate discounts to customers with no credit agreements necessary. All costs are upfront, nothing hidden, and there’s no need to have any risk tied up with your new bed.

Even if there’s nothing that tickles your fancy, if you’re in the market for a new bed then we highly recommend that you shop around independent retailers who don’t offer interest-free credit because the price you pay will likely be closer to the price it should be. Below are handy guides to show what to expect at different price points when buying a new mattress. The components, upholstery and spring units are all based on not taking interest-free credit. If you’re buying on credit you need to reduce the specification of the mattresses in each budget point to account for the hidden fees.

- What to expect from a £500 Mattress

- What to expect from a £750 Mattress

- What to expect from a £1000 Mattress

- What to expect from a £1500-£2000 Mattress

- What to expect from a £2000 Mattress

When you choose interest-free credit you’re paying for it. If you don’t use it, you’re paying for it. With our experience, you’re better off spending your hard-earned cash on what’s inside the mattress rather than finance agreements eating away at the quality of the mattress you’re buying.

Our handy guide below will show you exactly what to expect for your budget when buying a bed without interest-free credit. If you’re buying on interest-free credit then you can deduct up to 15% of your budget off the contents of your mattress.

| How much to spend on a double mattress? | What can I expect for my money? |

|---|---|

| Under £500 | Will not get you much at best a 13.5 gauge open coil/cage sprung with a thin polyester layer or a solid foam mattress. |

| £500 | Entry level spunbond springs with some form of synthetic upholstery. Usually one sided mattresses. |

| £750 | The beginnings of a basic pocket springs unit with 800 – 1000 count. No substantial amount of filling other than foams and synthetic materials. Two sided models. |

| £1000 | Should get you away from most low ranges and into the mid-range pocket spring models. |

| £1250 | Should get you a decent pocket sprung mattress with some Natural Fibre content. |

| £1500 | Should get you many manufacturers mid-range models with Natural Fibres |

| £1500-£2000 | Should get you a Hand Made primarily Natural Fibre Quality Mattress |

| £2000+ | You should expect 100% Natural Fibres and Traditional Hand Made Construction Method. |

| £5000+ | A Bespoke Hand Made Sleep System, High-end Spring Units & Featuring the Worlds Most Luxurious Natural Fibres. |

Summary

We don’t offer or use interest-free credit companies. We do offer our Clearance mattress models which would be a better use of your hard-earned cash rather than rely on interest-free credit which you will inevitably pay through the nose for.

Looking for more information before deciding on your next bed? Head to our Understanding Beds section for everything you will ever need to know about beds, mattresses, bases and headboards.

Why not call our small friendly team who can help provide recommendations based on your budget on 0161 437 4419?

Dreaming of the perfect nights sleep?

Ask us a question

There are over 6000 questions and answers submitted by you on all questions about mattresses and bed problems. Enter a keyword such as Vi Spring, John Lewis beds, bad back or Memory Foam and see if your question has already been answered.

If you can’t find an answer in knowledge hub, ask a new question. We aim to respond to all questions within one working day.

Newsletter

Enter your email to join our newsletter. We’ll send you occasional news and mattress expertise.